Walgreens wants to own the grocery fill-in trip by providing its shoppers with what it calls the “ultimate convenience” — defined as helping shoppers get in, get what they need and get out.

Kantar Retail assesses trip missions and cross-channel behaviors to examine how the Walgreens shopper may respond to this strategic goal.

Recently, Walgreens has been reinforcing the idea that it wants to own the grocery fill-in trip. With 75% of Americans living within five miles of one of its 8,200 stores nationwide, Walgreens is well positioned to provide accessible pharmacy and health care services to shoppers, as well as easy access to 18,000 household, food, beauty and over-the-counter health items — making it highly competitive with the likes of Walmart in terms of consumable products.

The “ultimate convenience” pillar of Walgreens’ U.S. retail pharmacy three-pillar strategy (rounded out by “offer best customer loyalty” and “deliver extraordinary customer and patient care”) focuses on providing shoppers with convenient locations to get in, get what they want and get out.

For better or for worse, health and wellness needs — in the form of O-T-C purchases, access to pharmacists and prescription plans — are what drives many shoppers to Walgreens. However, Walgreens wants to make a true difference in convenience overall, not just in terms of health-related trips but by providing more product choices, more specialized services and more digitally integrated solutions in an effort to position the retailer as a viable grocery fill-in destination.

To properly evaluate whether Walgreens will be able to convince shoppers to see it in this light, we must first understand the trip types Walgreens shoppers are currently making, the motivations behind those trips and the outlets to which they are making their fill-in trips today.

Walgreens shopping trip

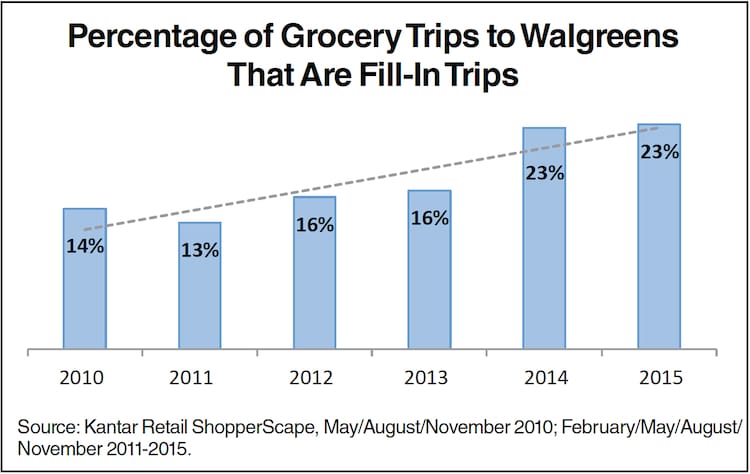

While the percentage of grocery fill-in trips to Walgreens has grown over the years, Kantar Retail ShopperScape data shows that grocery trips to Walgreens are most likely to be targeted trips for specific sale or coupon items. Fill-in needs motivate just under one-quarter of grocery trips to Walgreens — roughly the same percentage of trips that are motivated by immediate-use needs.

Therefore, thinking beyond the fill-in trip and in terms of all “quick trips” in general — i.e., trips made primarily to satisfy fill-in or immediate-use needs — the story changes a bit. In this light, the quick trip actually is the most common type of grocery trip to Walgreens, making up just slightly less than half of trips (47%). This, combined with the growth of the fill-in trip alone, suggests that Walgreens shoppers would welcome increased access to a quick, fill-in destination — assuming that the assortment is right.

Rite Aid acquisition impact on Walgreens’ fill-in trip

In October 2015, Walgreens Boots Alliance Inc. announced a $17.2 billion deal to acquire Rite Aid and its 4,560 stores. The deal, which is expected to close in the second half of 2016, means that the combined U.S. entity will have nearly 13,000 U.S. stores (pending a Federal Trade Commission divesture ruling). Rite Aid stores will keep their banners initially, but over time Walgreens plans to create “a fully harmonized portfolio of stores.”

This deal could not have come at a better time for Walgreens, given its quest to be the top fill-in trip destination. ShopperScape data shows that Walgreens wins a higher percentage of quick trips relative to the rest of the drug channel, making the retailer well positioned to evolve into a more comprehensive grocery fill-in destination for drug shoppers. However, taking on this endeavor is not without complications — and competition.

Threats to “filling in” at Walgreens

Retailers and channels focused on convenience and/or everyday-low price (EDLP) attract a sizable share of Walgreens shoppers. Walmart is the top cross-shopped retailer among Walgreens shoppers, and Walgreens shoppers are about equally (in fact, slightly more) likely to cross-shop the dollar channel as they are to shop Amazon.

The dollar channel’s threat is even more pronounced when it comes to shoppers of newly acquired Rite Aid. Rite Aid shoppers are more likely to shop the dollar channel than either Amazon or Walmart.

When it comes to dollar, in addition to these high rates of cross-shopping, the threat to the fill-in or “quick” trip to Walgreens is further compounded by the fact that the majority of trips to dollar stores are quick trips — i.e., fill in or immediate use. Especially when it comes to Family Dollar and Dollar Tree, Walgreens and Rite Aid shoppers who also shop these two dollar retailers are more likely than average to make quick trips there.

According to Walgreen Co. president Alec Gourlay, half of the retailer’s customers shop the store daily for milk, bread and other fill-in groceries, while another quarter look for on-the-go food. These shoppers want convenience, but they are still likely to understand the price environment for food and other consumables.

As EDLP and convenience-oriented retailers such as Walmart, Amazon and dollar retailers continue to improve their health care services, widen their grocery area and expand store locations, Walgreens could grow more susceptible to fill-in cross-shopping at these retailers.

Kantar point of view

Walgreens wants to become unique within the channel. To accomplish this goal, it plans to deliver a front-store vision through assortment, more exclusives and an increased focus on health and beauty. However, with the acquisition of Rite Aid and its 4,560 wellness-format stores, Walgreens will have the unique ability to deliver both convenience and health care to millions of shoppers.

Over the past few years, Walgreens has expanded its mission to include capturing more of shoppers’ quick, supplemental fill-in trips. ShopperScape data suggests that Walgreens is well positioned to capture the fill-in trip within the drug channel.

However, this focus on the fill-in trip — and especially on fulfilling needs in consumables categories — means Walgreens is now competing directly against a broader range of channels and box sizes. That competition set now includes Amazon, dollar stores and Walmart — including its smaller-box (40,000-square-foot) consumables-focused Neighborhood Market format. Given the high degrees of cross-shopping among Walgreens (and Rite Aid) shoppers into Walmart, Amazon and dollar stores, Walgreens is more susceptible to leaking fill-in trips to these “value first” retailers and must figure out a way to close the pricing gap.

While Walgreens is the quick-trip destination within the drug channel, Walgreens’ appetite is bigger than that. It wants to be the fill-in trip retailer. If Walgreens intends to reconfigure itself to achieve this goal, it must reevaluate its pricing strategy to be more competitive with EDLP retailers and find a way to simplify the complexities of health care for its shoppers.

Providing ultimate convenience is critical and building baskets with fill-in trips is profitable, but Walgreens’ equity is in health. Its biggest challenge will be to deliver in both a competitive and a nuanced retail environment.

Brian Owens is a director at Kantar Retail, where he leads syndicated drug channel research.

{kind=link}