Retail in the future will look nothing like what we see today. A new role for physical retailers is long overdue, and only a few have satisfied the need for change.

Mark Mechelse

Historically, one of the primary challenges facing North American brick-and-mortar retail pharmacies and their suppliers has been the inability to encourage shoppers to purchase more nonfood health and wellness products when they fill prescriptions.

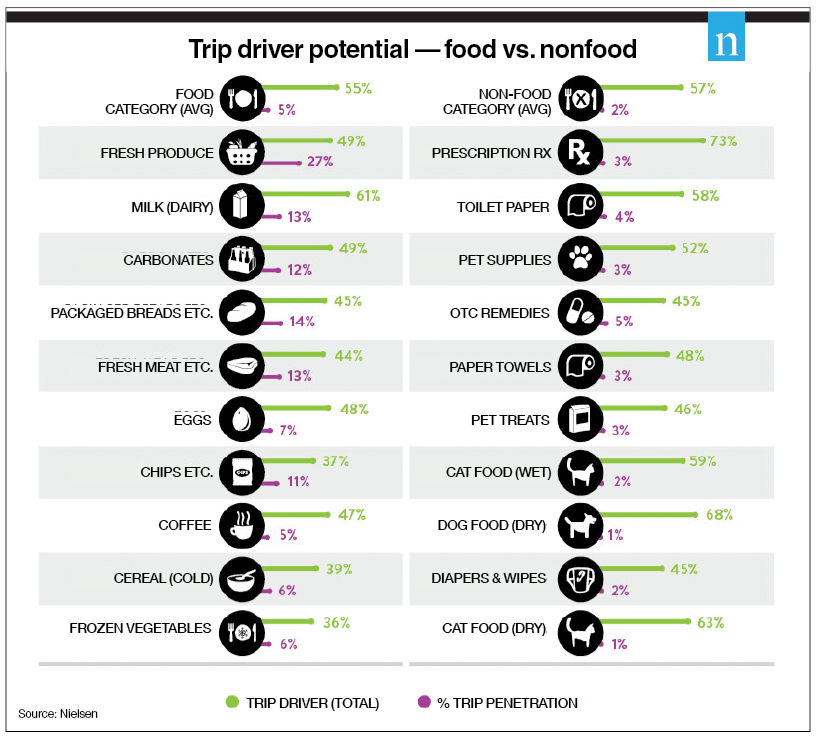

Astonishingly, out of 73% of the shoppers filling a prescription as their primary trip into a store, only 3% purchase other items during the same visit. This means retailers face a massive opportunity gap to close additional sales that are top-of-mind in the health care space.

At first glance, the 2016 Nielsen research (below) indicates that the issue to convert shopper missions while in a pharmacy would seem easy to resolve. After all, consumers want help. Time-pressed shoppers are constantly looking for efficient ways to accomplish more with each visit, and when they cannot find top-of-mind items they go online.

In a national study by WSL Strategic Retail, 57% of women, ages 18 to 70, said they “shop differently to simplify their life.” Forty-seven percent said they “will travel a little farther for one-stop shopping.”

Today’s “whole store” needs should be approached in the following ways:

Retailers want it. As pharmacy margins have declined with the Affordable Care Act, and overall margins have been challenged due to increased retail and online competition with reduced reimbursement rates, retailers recognize the importance — and urgency — of encouraging pharmacy customers to shop the whole store.

Manufacturers want it. They understand the value of the relationship between retailers and their pharmacy customers, and the opportunity it provides to grow sales of other products in the store.

Consumers must lead the way. In place of a “disease state management approach” a consumer-centric approach would develop a healthy shopper reputation in the following ways:

• Base retail communications and store design on how consumers manage their medical conditions.

• Eliminate in-store silos by focusing on motivating and aligning all department heads: pharmacy, O-T-C, general merchandise and produce/grocery.

• Identify appropriate and relevant healthy products throughout the store that are highly relatable to the local community.

• Present the pharmacy as a health and wellness boutique.

• Add more surrounding space to the pharmacy to provide an opportunity for pharmacists to direct shoppers to an effective center or aisle.

• Reemphasize the health experience as the store journey. If businesses do not interpret a good customer experience, they will quickly confuse it with customer service, but the two are very different.

It is important for retailers to recognize that, at this very moment, there are consumers making retail purchases in Seattle, Beijing and Sweden without engaging with a single clerk. Jeff Bezos is leading the shopper into a person-less store. That means emphasizing the health journey and identifying with the shopper is mission-critical to retail survival. In fact, it’s the key differentiator for all North American retailers.

Retailers and suppliers must acknowledge the consumers’ view of their conditions, rather than their own tactical needs. It is also important for retailers and manufacturers to fully understand the barriers to success across channels, and internally within their own organizations. By reorienting thinking, retailers, wholesalers and supplier partners will be better positioned to develop an innovative and manageable “whole store” approach based on consumer “connectors” between pharmacy and products throughout the retail unit.

The innovation of this approach lies not only in identifying and addressing the barriers to success but also in the selection of “high value” medical conditions as the core of in-store programs. High-value medical conditions must be evaluated as sales dollars, number of scripts, the prevalence in the market area and other measurements. Once identified, then the consumer purchasing “connectors” of these conditions need to be determined. The result is a program based on consumer behavior, validated by extensive data that creates a positive interplay between the pharmacy department and the whole store, to the benefit of both.

Now that we’ve come to understand that the core mission of the grocery and drug channel is health and wellness, those that offer the right assortment will ultimately grow, while others fall behind. In-store product selection must be reflective of the changing needs and mindset of consumers and their personal objectives to be healthy and feel good about their bodies.

Therefore, food as medicine is a way of living longer, whether a consumer is suffering from acute or chronic conditions. The more a pharmacy engages in front of the counter and acts as a guide to shoppers to complement their health journeys, the more relevant retail becomes. Shoppers trust their pharmacist’s advice more than their own family physician, according to recent studies by GMDC partners. As pharmacists move from behind the counter and engage with customers, the experience and loyalty-building factors come into play for those shoppers to return. To further enhance the in-store experience, retail dietitians, nutritionists and beauticians are also trained and deployed into select markets by leading retailers. This personalization is something that online retail is not able to provide.

A.T. Kearney has been tracking consumer behavior, working in tandem with GMDC to launch a series of reports on health and wellness trends. Recent findings suggest an increased expenditure and growing interest in health and wellness, even among mainstream consumers. This is having a profound effect on the sales of natural and organic products, since today’s consumer is savvy and will shy away from products with unpronounceable ingredients and indiscernible processing practices. With recent economic factors, the industry will likely see strong discretionary incomes allowing trading up to specialty and premium products, where natural products are primarily offered.

Let’s not forget that the thrust in fresh food demand is also increasing, recently measuring 49% in dollar growth against all categories in the store, according to Nielsen. It is expected to continue to surge in the near future based on GMDC’s anticipation of the ever-growing health and wellness-minded consumer and the self-care road map that retailers are trying to navigate. As the fresh food movement continues to gain in popularity, stress will be put on other categories and space within stores, especially as new store sizes continue to shrink and assortments are optimized and curated toward the localized shopper.

As more consumers eat fresh, we may see certain supplements and energy drinks under some pressure. Consumers will also gain an increased awareness of the preventative measures they need to take with their own health, simply by experiencing the positive effects from healthy eating. Preventative and enhanced services inside the food channel will create hotspots, in both urban and rural areas, and will be a future driver that ultimately brings much-needed foot traffic back to physical outlets. As assortments are optimized, and more space is made available in the existing big boxes, Best Buy has become a “next practice” model for those who are looking to enhance offerings.

The tug-of-war occurring inside brick-and-mortar retail is real. As certain categories leak online due to delivery, subscription and convenience models, retailers must realize that the shifts they are experiencing are forcing a redefinition of trip missions. Shoppers want to be healthy and lead lives in which they have full awareness of the things they consume. The food and drug destinations have the unique ability to act as self-care providers, saving time and money while creating education for consumers to lead the lives they aspire to. With 48 million consumers over the age of 65 (and this segment growing at 3.4% year over year) and 74% of consumers using vitamins to promote their health conditions, a health and wellness mindset is no longer in a niche position. As retailers recognize this, the innovators will design stores around consumer health experiences and make the pharmacy an integrated space at each location, identifying key self-care categories that drive customers back into their stores.

Retailers have the unique ability to chart interactions and support communities in ways other providers cannot, while filling the fundamental mismatch between online and local retail that consumers are seeking.

Mark Mechelse is vice president of insights and communications at Global Market Development Center (GMDC). He can be contacted at mmechelse@gmdc.org.

{kind=link}