The high value of pharmaceutical shipments has traditionally meant that all parties in the chain drug industry were primarily concerned with quality. They needed a reliable, transparent solution. Given that shipping represented a tiny percentage of drug costs, price was a lesser concern. But recently shipping rates have increased sharply. Is there anything the industry can do?

Michael Zimmerman

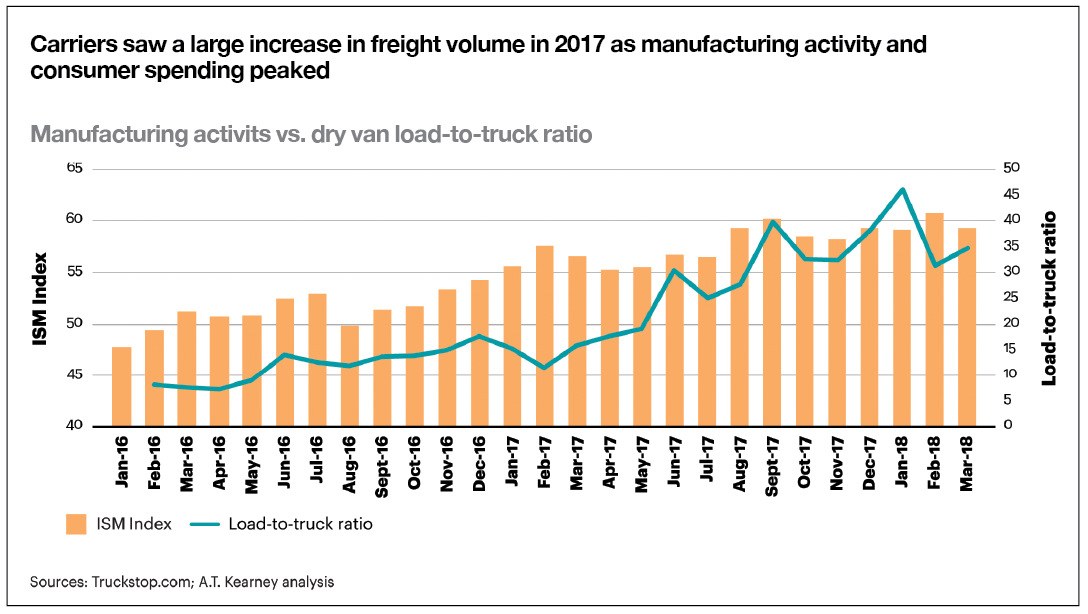

In 2017, dedicated trucking costs increased by 9.5% over the previous year. These higher prices, A.T. Kearney’s “2018 State of Logistics Report” showed, resulted from increases in freight volume and restrained supply. With a rise in manufacturing activity and consumer spending, the economic momentum that lifted gross domestic product in the United States by 2.9% in 2017 is likely to continue.

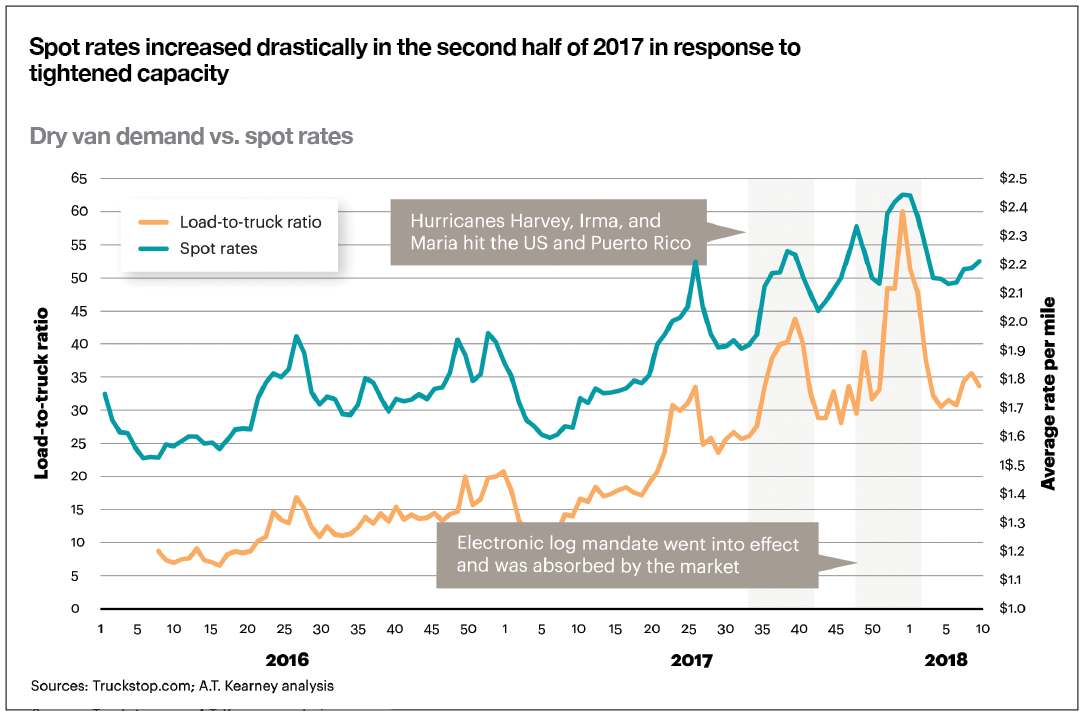

Meanwhile, capacity is tight. Critical events in 2017 included hurricanes and new mandates for electronic logging devices in trucks. And fundamentally, it’s difficult for supply of trucking capacity to expand to meet this higher sustained GDP growth because of a driver shortage that has been years in the making. With unemployment low, and driver poaching between carriers high, carriers struggle to attract and retain recruits. Carriers have raised driver compensation by 15% to 18% since 2013, according to the American Trucking Association — still not enough to attract new drivers in sufficient numbers.

Thus the capacity crunch is likely to continue. Swelling inventories and tax changes will boost economic performance (although fears of trade wars cloud the outlook). Driverless trucks at more than 10% of truck volume are three or more years off. Supply chain and logistics leaders can’t merely hope the problem will go away.

A big squeeze comes from the dedicated trucking sector. For example, due primarily to its dedicated contract services segment, J.B.

Todd Huseby

Hunt’s first quarter 2018 revenues rose 20% and operating income rose 13%, compared to the year-ago quarter. Likewise, with more freight in higher-rate categories, Werner’s first quarter net income rose by 74%, and with high demand for premium services, refrigerated hauler Marten was up 26%.

These dedicated and premium categories have been the exclusive home for prescription drug shipments. Many pharmaceuticals need the temperature controls, on-time performance, transparency and quality assurance of a dedicated carrier. Switching to common carriers or brokers would mean less control over conditions, increasing risk. Given the high value of pharmaceutical shipments, those risk/cost trade-offs have rarely seemed worth considering.

But solutions do exist. Other industries have addressed these trade-offs. Manufacturers of bulky items, where shipping represents a far greater percentage of sales, have long-standing programs in place. More recently, other manufacturers have adopted programs by necessity.

The key is segmentation. You can segment by customer, shipment or carrier to understand the needs, constraints, limitations and costs of each. For example, a food distributor identified its most critical inbound shipments and ensured that those were handled by either its dedicated fleet or its most trusted common carriers. Meanwhile, it allowed less critical shipments and lanes to be handled by brokers. By doing deeper analysis and setting expectations, you can expand your available options without sacrificing service in critical segments.

One approach that many of our clients have used is collaborative optimization, a software tool that helps assess a shipper’s list of requirements or constraints against a variety of carrier offers. The goal is to find the combination where both companies can benefit, from proposed discounts, realized network needs, and capacity and volume commitments.

Algorithms provide a starting point for conversations. In a world of complicated optionality, you can understand trade-offs, see comparative advantages and create win-wins. With investments in collaborative optimization, you can better allocate scarce capacity and mitigate risks while better explaining and exploring trade-offs with your stakeholders.

Perhaps the most valuable approach is to examine the extent to which you are a shipper of choice. Making yourself a shipper of choice is a valuable strategy, because when a carrier is faced with capacity shortages, it treats attractive shippers more kindly than the rest or, to put it bluntly, “fires” the shippers that are hard to do business with.

Improved planning and communication — including forecasting load requirements by site and lane, being able to accommodate both drop trailer and live-load shipments, and giving carriers more flexibility on their appointments — are shipper-of-choice practices that enhance shipper-carrier relationships.

Despite the capacity crunch giving carriers more power in the relationships, they remain a two-way street. Leading shippers are devoting more energy to address drivers’ and carriers’ pain points — minimizing drivers’ waiting time, providing well-appointed waiting rooms and even intervening with customers to the same ends. At the same time, they won’t do this for every carrier, only the ones that best meet their performance, capacity, transparency, pricing and other key goals.

Finally, you can increase your internal investments in capabilities for shipping management. These may include strategic sourcing, carrier assessments using key performance indicators, and improving processes for how you audit and pay invoices.

Such tools may be familiar from your other supplier relationship management efforts. In effect, you are acknowledging that the increases in transportation costs have elevated your carriers to a level equivalent to some of your other significant suppliers — as relationships worthy of attention and even affection.

The increase in shipping costs won’t go away. That makes it a threat to long-term profitability. But because the effects of this increase are being felt industrywide, well-organized companies can also see it as an opportunity. By deploying proven methods and tools — some that are advanced and some that are quite basic — they can reduce costs and improve service and profitability to outperform their competitors.

Michael Zimmerman and Todd Huseby are partners at A.T. Kearney. They can be contacted at michael.zimmerman

@atkearney.com and todd.huseby@atkearney.com.

{kind=link}